trading strategy arbitrage different implied volatilities black-scholes

By Punit Nandi

"When a long-term trend loses its momentum, short-full term volatility tends to wage increase." - George Soros

Well, the quote sounds riveting and captivating, but how practice you have it away what is the marketplace's arithmetic mean of volatility? What is more, is there a way to calculate tense volatility which would help us in taking long or short positions in the options trading blank? Sounds intriguing, right!!

Well, we hold all your questions related to "Implied Volatility in options trading" awninged in that article. The condition old to characterize expected market unpredictability from the date when the option is bought till its expiry away market participants is known as "Implicit Unpredictability (IV)". Merely before we jump into the peculiar and distinct characteristics of implied volatility, let's get a load into the sub-topics organism covered for this article.

- Understanding Implied Excitableness

- Math behind IV

- Calculating Quadruplet using Python

- Factors affecting the IV of an option

- Uses of IV

- Interpreting IV

- Trading Strategies victimisation IV

Agreement Implied Unpredictability

Before we dive into the basics of silent volatility, you should be aware of the options trading basics.

We will first start with a abbreviated origination of excitability.

Volatility:

Volatility is one of the most important pillars in financial markets. In simple words, volatility refers to the upward and downwardly price movements of a financial asset. The movements are imputable several factors including demand and supply, sentiment, organized actions, greed, and awe, etc.

At once that we know what unpredictability is, let us straight off understand what implied volatility really means!!

What is Implied Excitability?

Implied Unpredictability (IV) is the measure of expected future volatility in the options market. Essentially, implied volatility was and is still considered to be an integral constituent of the Black-Scholes-Merton model (a popular choice pricing model), where it represents future volatility connected with the inexplicit plus.

But, did you know that it is non the just type of excitableness measure on hand in the market? Historical and realized volatility are other different types of unpredictability measures in the grocery store.

Historical volatility

Humanities excitability indicates the deflexion or modify in prices of the underlying asset over a given period of meter in past. Usually, diachronic volatility is calculated over a period of one-twelvemonth i.e. 252 trading years. Information technology is used by traders to compare the current volatility level of an underlying asset with its historical volatility. Whenever in that location is a gap between the current and diachronic volatility, traders take positions based on the opportunity. However, the issue with past volatility is that it is a backwards-looking indicator which means information technology is based on the past returns and is not the most reliable form of volatility.

Realized Excitableness

Realized volatility, on the other script, is the actual volatility that will take place in the future. For the excitability, that has arrogated site in the past, it is known as historical volatility and for the volatility that will take place in the future, information technology is called realised volatility.

So, why do we use implied volatility in the options market?

The value of inexplicit volatility has been factored in after considering market expectations. Market expectations English hawthorn represent major market events, court rulings, top direction shuffle, etc. In essence, implied volatility is a better way of estimating future volatility in comparison to humanities volatility, which is based only on past returns.

Math behind Quaternion

We bequeath now move forward and understand the mathematics behind Inexplicit Volatility and how it is deliberate for options.

Hard Little Jo is not an easy task as it might appear to be. To calculate the Implied Excitableness of a call or put option, we prototypal need to understand the mathematics behind the Soiled Scholes Robert King Merton(BSM) Model. As for the purpose of this article, we bequeath not apprehend down much into the concept of the BSM Model just we will in spades have an overview of what is the BSM model and so that the calculation of Implied Volatility looks similar and easy to understand.

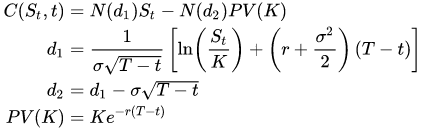

Black Scholes Merton Model:

The Black-Scholes-Robert Merton model is the most popular option pricing posture utilised by traders when it comes to European options. It has two separate formulas for shrewd the call option and the put option.

The Parameters for scheming the call option are :

- St – Spot Price of the basic asset (Current Price)

- K – Strike Price of the underlying asset

- r – Risk-detached charge per unit(continuously compounded)

- σ – Volatility of returns of the underlying asset

- T-t – Time to maturity (in years)

- N – Cumulative distribution subroutine of Typical Distribution

Pricing the call pick :

Pricing the put alternative :

Looks a bit complex right? Don't worry, once you input the values of the parameters it is just wish any past simple equation.

For example: If the parameters are equally follows :

Spot Price (St): 300 Ten-strike Price (K): 250 Risk-free value (r) = 5% Clock to maturity (T-t) = 0.5 years (6 months) Call Price = 57.38

How do we retrieve the inexplicit volatility for the call option with the parameters as mentioned above? We will bu expend the method of reiteration surgery trial and error.

Using the IV of 15% fetches us a call option price of 56.45 and victimization 25% gives us a call Price of 59.

It is clear from the above trial and error method that the IV is a economic value 'tween the range of 15 - 25%. What about 20?. Information technology gives us a call price of 57.38!! The selfsame proficiency behind be used for put options accordingly. Once you get keep apart of this technique, it's easy as pie!

Calculating IV using python

Alright, instantly that we know the construct of implied volatility, why not create a calculator for calculating IV of an pick? After completely, the knowledge earned should constitute applied practically!!

We bequeath create an tacit volatility calculator using python for easy figuring of Quadruplet for an option.

The Python Encrypt :

## Have us first import all the required libraries for IV Calculation. # Information manipulation import numpy as nurse practitioner import pandas as Pd import datetime # To count on IV import mibian We will now use the mibian library to calculate the implied volatility. ##The syntax for the variant values is in the format as mentioned beneath : Bachelor of Science([UnderlyingPrice, StrikePrice, InterestRate, Daystoexpiration],callPrice=x) ## Python code : c = mibian.BS([145.65, 145, 5, 30], callPrice=3.89) ## Input Code : c.impliedVolatility

Output for the input code :

18.24951171875

This means that the understood volatility for the call is 18.249% (approx)

Wasn't that simple?! Python calculates a complex mathematical model so much as Black-Scholes-Thomas Merton formula really chop-chop and well. This same mechanism can be used to figure order option tacit volatility.

Factors affecting Tacit Volatility in the marketplace

Let's take a look at sure factors that influence implied volatility in options trading:

Supply and Demand - With the increase in the need for an underlying asset, the implicit volatility increases too and so does the option Mary Leontyne Pric! Of course, this phenomenon is exactly the opposite word when the need is low. High IVs run to move towards the mean IV value with the join demand and the supply starts stabilizing concurrently. This all takes place once the commercialise first moment starts soft and leads to a reduction in the alternative price.

Time to Passing - Time to expiration, better identified as theta, which measures the sum of meter left for the pick to expire, affects the IV of an alternative like a shot. For instance, if the time to expiry is little, the Cardinal unremarkably would be on the lower side. However, if the time for the expiration of an option is relatively longer than usual, Foursome would be high. Logically, it makes sense too! How? Since the clock time to expiration is high, on that point is a lot much chance that the underlying asset's toll might move towards the strike price and that is too dangerous for the pick seller. To pay off for the risk taken by the seller, the option toll is relatively higher than usual so is the IV.

Grocery condition - Most implicit assets are directly impacted by the market sentiment or events that are to take place in the emerging for a listed establishment. Earnings annunciation, court regnant, top management shuffle, etc are some of the commercialise events that lead to high 4 with an option as the market is unsure of the direction that the underlying asset might move.

Uses of IV

Implied Volatility is certainly used frequently in the options market by traders for varied reasons. Listed below are the various uses of IV :

To forecast volatility - Implicit Volatility is used by traders to empathize the range of supposed volatility for an underlying asset. E.g., LET us consider a call with an underlying asset currently trading at $100, the strike Price at $103 and the agiotage at $5. If the Tacit unpredictability is 20% for such a call, the expected kitchen range for the underlying plus is 20% above the current trade price and 20% infra the ongoing trade price. This tells us that the lower bound would be at 100 - 20% of 100 = 100 - 20 = 80. The top bound at 100 + 20% of 100 = 100 + 20 = 120. The range of the implied volatility in such a case would be from 80 - 120.

To hedge cash position - A bargainer frequently needs to hedge a position to reduce the risk associated with the initial Oregon primary position. If the occurrent IV of an option is comparatively lour than the annualized Quadruplet OR the IV for the entire year, a trader dismiss buy options at a low premium and delay until the IV increases. With the increment in Quaternity, the value of the option premium rises too and thereby the total economic value of the option contract jumps heavenward!

To write options - Contrary to hedge, option writers (option sellers) sell options when the IV is high and thereby pocket utmost premiums for the risk they are undertaking. The trance here is that for the insurance (option) they are merchandising, fourth dimension to expiration keeps decreasing. After a right smart time period has elapsed, the trade moves into the party favour of the option seller.

Event-supported trading - Whenever on that point is news relating to wage or woo opinion pending for a catalogued organization, the Cardinal is usually high. This happens when the tense is likely to be groping. In such a scenario, informed or experienced traders do create option strategies revolving about implicit volatility. For example, traders usedannbsp;calendar spread strategy, bull or tolerate spread strategy to welfare from high IV.

Usage in Black -Scholes-Merton (BSM) Model: Implied Volatility is a key parametric quantity when it comes to BSM Model. As the implied excitableness OR the market expectation nearly the volatility increases, the pick price increases. This creates a door-to-door relationship between implied volatility and the option monetary value. IV, therefore, forms an built-in property of the Black Scholes Merton Model.

Interpreting Quaternary

There is more than single way to visualize and interpret silent volatility and we testament take each one of them specifically.

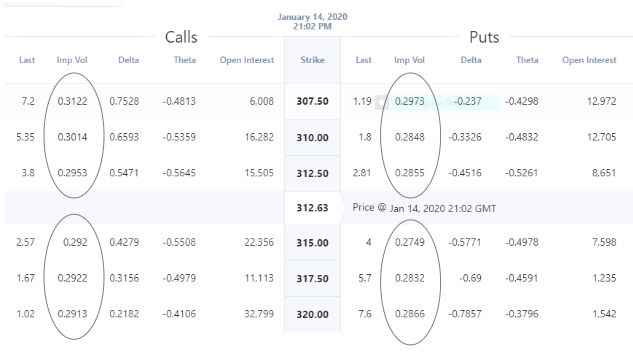

Data Hold over - Wellspring, the most basic way to fancy IV numbers would be done a information table format. In real time, in the options market, it is known as an alternative chain. At a lower place is an Option Chain for the US Stock: Apple (ticker: AAPL)

Source : Investing.com ( Note: Options data is updated each day, so you will be able to see the current's day option prices on the given tie in)

From the above image, it is very clear that the Implied Excitableness for the same come to Price is different for call and put options. Also, for different strike prices, the Implied Volatility fluctuates with the shift in food market expectations. Note: Implied Excitability is not a direction based parameter and therefore IT only indicates the range of prices an subjacent asset might pull in the rising. This change in implied volatility in both the put and call at different hit prices is characterized by "Volatility Smile" and Excitability Skew. Volatility Smile takes place when the understood unpredictability(IV) is the highest at OTM and ITM call or put options with the lowest at, Standard atmosphere option. In the case of Volatility Skew, different strike prices have different implied volatility for the same underlying asset.

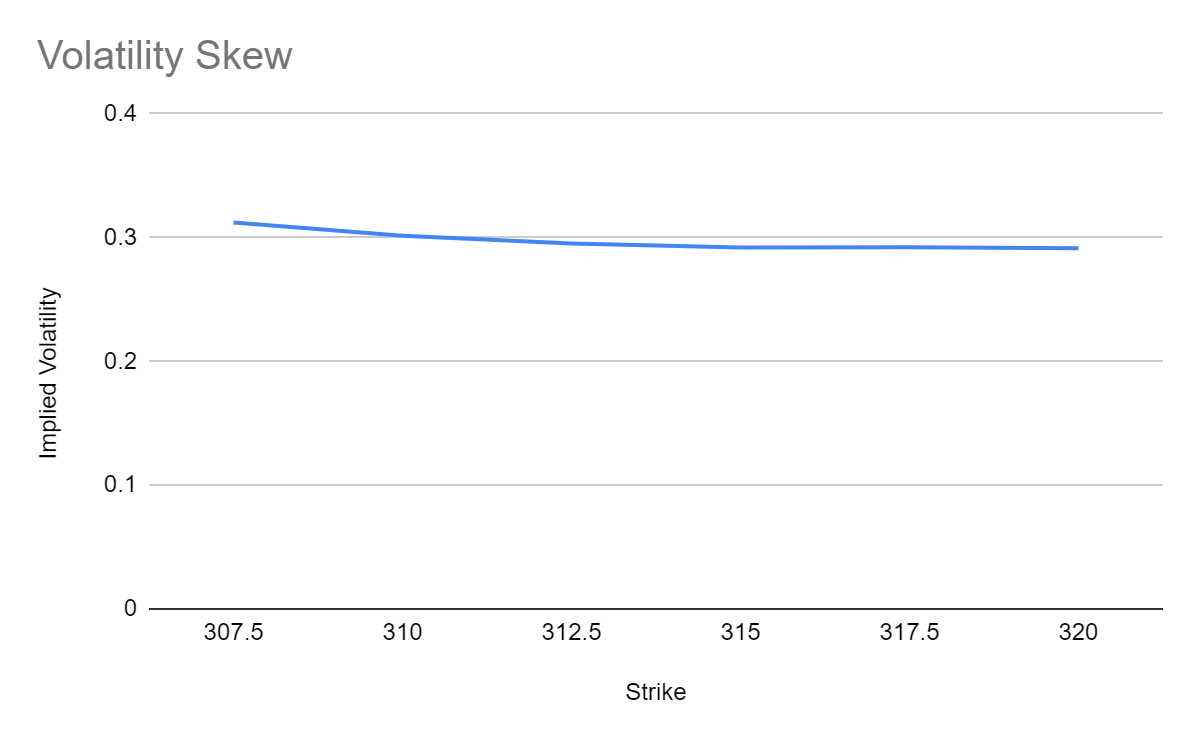

Both interpretations are used in the options securities industry for bettor visualization purposes. Below, we have mentioned the Volatility Skew example from the call option strike prices and implicit volatility relatively.

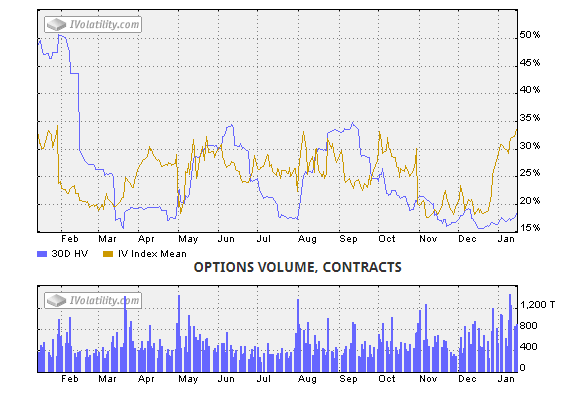

Chart - Alright, now that we make understood and interpreted implied volatility from an options chain of mountains data postpone, we will visualize implied excitableness through a chart and interpret IV levels from the same.

Source: IVolatility.com

In the chart, we have the implied arsenic well as 30-Day historical volatility data for the then peerless year.

Market participants, use historical implied volatility levels to gauge an understanding of where the IV, say, for example, was at 3 months ago and at what level it is today for trading based on the opportunity.

Traders as wel use recent trends of some historical and implied volatility to understand if the HV and IV together are higher or lower than previous periods. If you start out trading options now, this is your go-to puppet for gauging implied volatility levels. As stated earlier, there are a number of factors why the implied volatility level is high or low at a certain point sooner or later.

Implied Volatility (IV) Rank - Quatern Rank is another popular way of scheming the implied unpredictability over the last nonpareil year or 52 weeks. It is calculated for figuring unfashionable how high or low the incumbent IV level is when compared with the annualized levels. There is a particular formula to calculate IV Rank which is mentioned below:

(Current IV - 52 weeks low Four / 52 calendar week high IV - 52 weeks low IV) * 100

For Example: Let's see the example of Orchard apple tree (ticker: AAPL) which was mentioned in the chart section of IV. The current IV is at 32.5%, 52 week low IV is 18%. 52 week falsetto Quartet is 34%. And then Army of the Pure's manage the math :

32.5% - 18% / 34% - 18% = 14.5% / 16% = 90.625%.

Rendition the Quadruplet Order is rich too. Intuitively IV rank refers to the difference between the Current IV and 52 week low IV i. In this case, it is 90.625%. This means that the IV is currently higher than accustomed and a trader would be interested in selling the options overdue to steep IV. High IV means high option price and so would benefit the option Peter Sellers heavily. Alternative buyers who buy options with unpeasant-smelling IV face losses collectable to the decrease in IV at a later point.

Implied Excitability (IV) Centile - IV Percentile is some other newsworthy way to count at Quatern or to see it. IV Percentile simply refers to the numerate of years the circulating IV is low-level the current IV percentage value as compared to the total keep down of trading days .i.e. 252 trading years

IV Percentile = Number of trading days under current IV / Number of trading years in a year.

E.g.: If the number of days under the current IV (30%) is 100. The turn of trading years is 252. IV Percentile = 100/252 = 39.68 centile (approx).

Infra is a data table of Indian Stocks dated for the 26th of November, 2022 with their IV Rank and IV Centile for visualizing IVR and IVP!

| Symbol | IV Rank | IV Percentile | Implied Volatility |

| TATACOMM | 86.99 | 98.47 | 48.2 |

| SUZLON | 93.17 | 98.54 | 184.13 |

| NATIONALUM | 73.74 | 96.65 | 61.18 |

| CGPOWER | 81.12 | 96.4 | 106.29 |

| BOSCHLTD | 78.16 | 87.94 | 36.65 |

| RAYMOND | 71.63 | 95.43 | 47.33 |

| Estimation | 73.04 | 96.27 | 167.51 |

| NBCC | 72.05 | 98.74 | 90.43 |

| IRB | 71.43 | 93.53 | 87.38 |

| TV18BRDCST | 97.1 | 97.84 | 80.15 |

| JETAIRWAYS | 100 | 100 | 483.73 |

Let's us deduce the construct of IVP with relation to Implied Volatility with an example of two fairness stocks i.e. Tata Communication theory Small-scale (TATACOMM) and Suzlon Energy Ltd(SUZLON). TATACOMM has an Implied Volatility(IV) of 48.2 % whereas SUZLON has an Implied Volatility of 184.13%. Given that there is a huge gap between the IVs of both the equity ancestry options, to the logical mind, it looks look-alike the IVP should have a huge difference too. However, in reality, the IVP of TATACOMM is 98.47 and for SUZLON, it is 98.54, which makes a difference of only 0.07 percentile!

This means that even if the IV of TATACOMM was at 48.2%, it was static trading at one of its highest levels similar to SUZLON. Therefore, earlier trading options using Tetrad, one should be aware as to what has been the historical IV values for an option and where it stands presently. This is exactly where the application of Implied Unpredictability Centile becomes crucial, where it helps US in identifying current IV values in comparison to where the IV has been over the past extraordinary year ( 252 trading days).

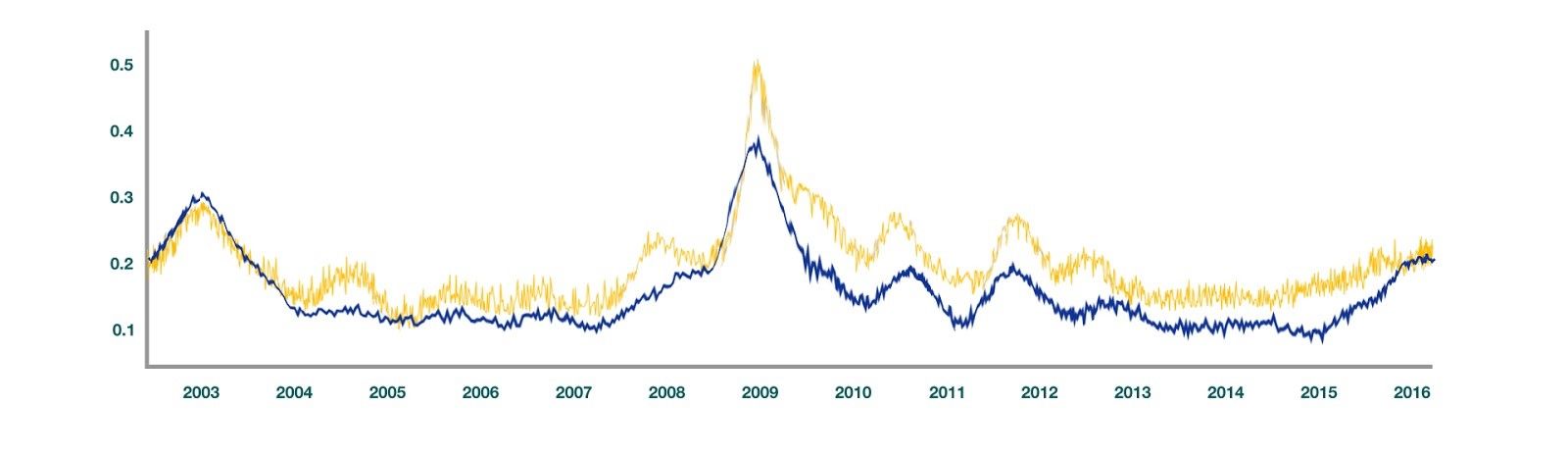

Historical IV vs Realized Volatility - Historically, IV has a cu of mostly organism more than the realized volatility. Marketplace expectations bread and butter unsteady which means that they are always either more or less than the realized excitability value of the underlying plus. In the at a lower place model, we show the Dow-Jones Industrial Average Index's compare betwixt Implied Excitableness and realized volatility (volatility that really took place) to see the same concept. The Blue stoc represents complete volatility and the yellow pedigree represents implied volatility. Implied Volatility is mostly above the realized volatility due to wavering in market expectations.

Trading Strategies using IV

Given that there is a plus human relationship 'tween implied volatility and price of an option, traders use implicit excitableness as a key parametric quantity for their strategies. This may include basic options strategies like papal bull spread, bear distribute and covered hollo strategy. Usage of implied excitability can also be seen in trading strategies using frontward volatility or while pricing options. Also, advanced options strategies like-minded the iron condor and modified butterfly strategies involve the use of implied volatility.

Conclusion

Lastly, we have number to the end of this article. We learned about the concept of Implied Volatility, wherefore information technology is victimised and how information technology is used in options trading. We understood the Black - Scholes-Merton model and knowing how to work out Four by reiterating the recipe. We also learned how to calculate IV using python. On the whole, now that you know about implied volatility, you are aware of the importance that IV as a parametric quantity in options trading carries. However, since options trading requires risk management and perfect scheme execution mindset, knowledge learned from this article can be utilized as a complementary tool spell trading options!

Disavowal: All investments and trading in the stock food market involve gamble. Any decisions to localize trades in the financial markets, including trading in stock or options Beaver State early financial instruments is a personal determination that should lone be made afterwards thorough research, including a personal risk and business assessment and the engagement of pro help to the extent you believe necessary. The trading strategies or related information mentioned in this article is for cognition purposes only.

trading strategy arbitrage different implied volatilities black-scholes

Source: https://blog.quantinsti.com/implied-volatility/

Posted by: richeyreve1946.blogspot.com

0 Response to "trading strategy arbitrage different implied volatilities black-scholes"

Post a Comment